Investing in DeFi - Part 2: How do I DeFi?

Investing in DeFi - Part 2: How do I DeFi?

I explain multiple ways to invest in DeFi and evaluate them against the framework I defined in part 1

In today’s post I continue the DeFi journey by providing an explanation of 5 different ways to invest in DeFi and how they stack against my evaluation framework

In the next post I will journal the investment I make and share my decision-making process.

As a refresher, here is the framework I will follow as I evaluate investments

Do I understand how value if being generated?

Can I understand the sources of risk?

Is the upside predictable?

Is the product secure and reputable?

Are there likely regulatory risks?

How much maintenance will the investment require from me?

Let’s look at the potential investments

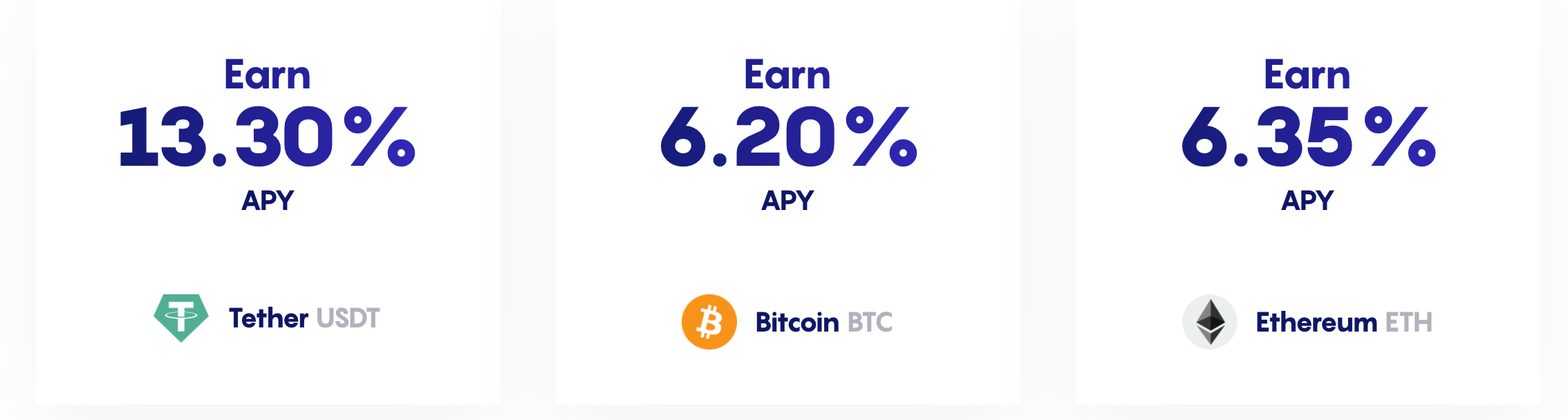

1. Crypto Lending

Crypto lending is conceptually simple. Using some kind of exchange, you provide loans to other individuals with your crypto currency. Borrowers provide their own crypto currency as collateral and the exchange dictates how much they can borrow based on the value of their collateral. Yields on crypto crypto lending vary quite a bit depending on the coin or token that you are lending.

There are 2 kinds of crypto lending platforms, centralized and decentralized

1.1 Centralized lending platforms

In a centralized loaning platform, the operator collects and holds your crypto currency and sets their own borrowing and lending rates based on market conditions. It’s not considered pure DeFi because you do not hold your own cryptocurrency and the transactions are not dictated my a smart contract that has the terms encoded into it. But the barrier to entry is low and you do not need a traditional bank account to participate. You will need to submit personal information such as your social security number, place of residence, and more1.

BlockFi and Celsius in the US, and Nexo in Europe are some of the better known and most reputable services.

1.2 Decentralized lending platforms

In a decentralized platform, there is no human operator setting the loan rates or approving transactions. Instead, supply and demand automatically dictate the loan rates. It is all handled through smart contracts. In a decentralized application, there is no requirement to identify yourself and you can control your own cryptocurrency keys. You simply connect your crypto wallet (I use Metamask) and decide where to lend funds.

AAVE and Compound are some of the more established decentralized platforms.

As a mere mortal, I struggle to find an obvious reason to prefer a centralized vs. decentralized platform. It may come to a personal decision on whether you trust humans or smart contracts more or down to which offers the best yield for the coin/token that you want to lend. So, for simplicity’s sake I will evaluate both approaches as one.

Lets evaluate crypto lending:

How is value generated? You loan your crypto currency and earn interest as the loan is repaid.

Risk: Most people are using these loans to leverage themselves and invest more aggressively. While platforms limit the borrowing to 50% of the collateral, if the crypto market takes a big dip (volatility is high and cycles comes with big swings) you risk losing your capital. Centralized platforms have more restrictive “lock in” requirements, with most services offering a free withdrawal per month, with fees after that. Generally you have more flexibility than with a typical bank.

As a simple mortal I feel uncomfortable directly lending my crypto for others to take risk with… I realize that’s how traditional lending works too, but I don’t love itUpside: Rates vary from less than 1% to 17% (how is this possible?!). Stable coins tend to have higher yields. Interest earn is compounded monthly. Rates change over time based on market conditions and need to be monitored

Security: Centralized platforms have security similar to payment systems or banks and seems pretty secure. Decentralized platforms could suffer from bugs in smart contract code or programmatic attacks. The larger platforms tend to have a high focus on security and my concern is low.

Regulatory: This is hard to predict. U.S. regulators tend to step in when a small set of actors can take unfair advantage of unwitting investors. I imagine that algorithmically driven lending platforms could be used to hide Ponzi schemes and other fraud, which could trigger regulation across the board.

Maintenance: Medium. Because rates can change over time or coin/token price can move quickly I would want to check in weekly or monthly

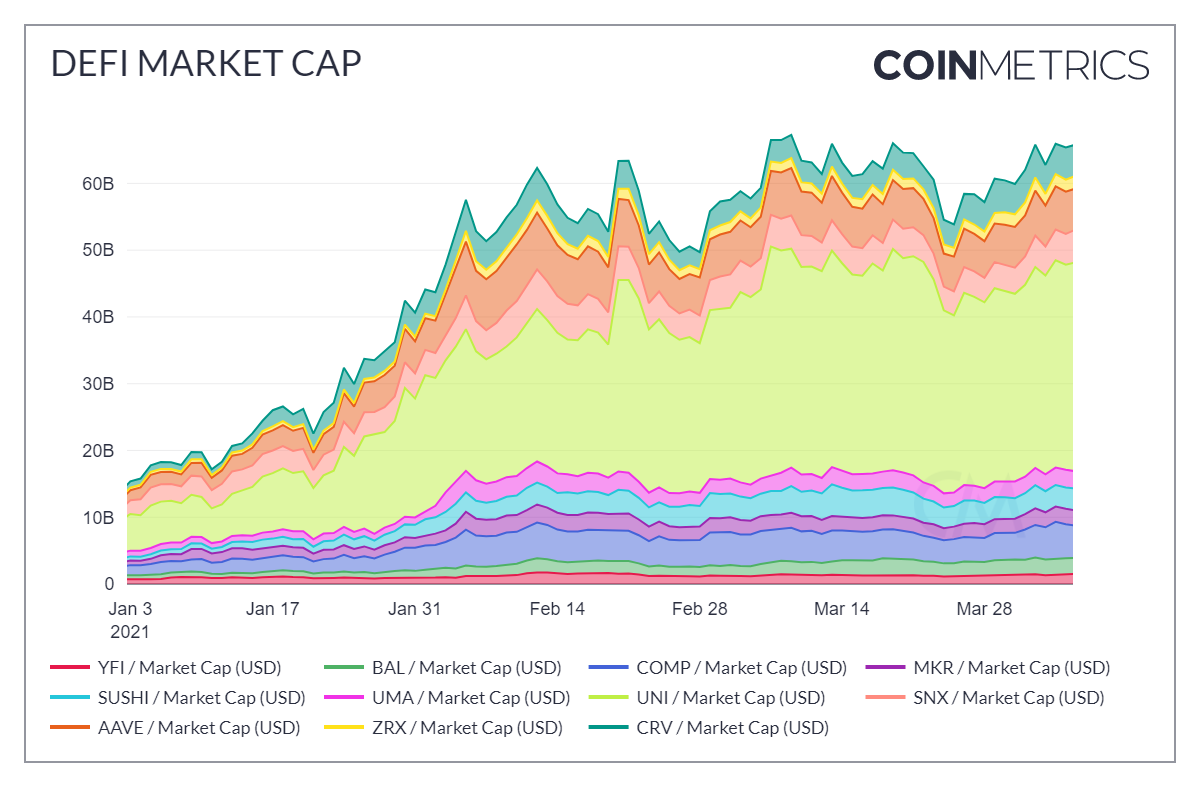

2. Direct token holding

While this approach does not typically generate passive income, it can be good way to get exposure to the gains in the DeFi space. Many of the lending platforms2 and exchanges3 issue their own tokens to facilitate faster operations and minimize some of the fees associated with layer 1 blockchains such as the dreaded Ethereum’s gas fees.

The value of the token is correlated to the use and adoption of the token for transacting. So if the hypothesis is that the DeFi space will continue to grow in users, capital locked in, and transaction volume, then these tokens should increase in value over time. The last few months have seen 2-5x increases in the price of some of these tokens.

It’s worth noting that some of these tokens will reward the holders with additional tokens generated by service fees or other mechanisms, so some may produce a small amount of yield.

Lets evaluate token holding:

How is value generated? Token adoption leads to higher demand and higher price. Some protocols will issue additional tokens to the holders.

Risk: Success is tied to the growth in transactions and total value locked in; similar to holding a cryptocurrency. The quality of the smart contracts behind the token’s platform could be a risk factor.

Upside: The growth of the particular token, but it’s hard to quantify.

Security: Depends on the token and the protocol it is associated with. Being built on Ethereum provides some peace of mind, other blockchains are less well tested. The token and protocol should also have a security audits performed to mitigate risk. Time since going live and total value locked in are good factors to consider… if there are billions locked in and no recent breaches it’s a sign security is good.

Regulatory: Some DeFi services and tokens carry a lot of risk, some are scams. Regulatory action as a result of a few bad actors could affect most tokens if applied too broadly (as is typical of regulators), which would drive down token value

Maintenance: Medium to High. It would be important for me to stay up to date on news for each of the tokens to ensure the service they are associated with is growing. I would also need to keep an eye on new entrants that could provide a better opportunity or drain a platform of its users by enticing them with a better product.

3. Investing in a DeFi index

A DeFi index is a managed investment where an investor allocates your capital across a portfolio of DeFi tokens. Investing in an index would provide a similar exposure to holding tokens but without the need to keep up with research or periodically optimizing allocation across various tokens. The downsides are fees (2-3% is typical) and no control over where the investment goes, so you could miss the next hot token.

So far BitWise is only one DeFi index that I am aware of. They have an advisory board that is constantly looking at the DeFi space, vetting tokens across a range of criteria and balancing the portfolio allocation monthly. In order to invest in the fund, you have to be a US person (citizen, green card or long term resident) and meet the criteria for an accredited investor — which mostly means you have enough net worth or income to take on the risk of this investment — and there is a minimum investment of $25,000.

Lets evaluate investing in a DeFi Index:

How is value generated? Token adoption leads to higher demand and higher price.

Risk: Success is tied to the growth in transactions and total value locked in; similar to holding a cryptocurrency. The quality of the smart contracts behind the protocol could be a risk factor, but is mitigated by the research and vetting in the fund.

Upside: Lower than direct token holding due to fees and potentially missed opportunities to invest in newer less proven tokens.

Security: Similar security exposure to holding tokens. However due diligence by the fund managers greatly reduces the security risk

Regulatory: As with tokens, regulatory action as a result of a few bad actors could affect most tokens if applied to broadly (as it typical of regulators). Fund managers specifically look for low regulatory risk. Their experience in traditional finance ensures they can gauge this risk better than me.

Maintenance: Low. The portfolio is rebalanced monthly, the fund managers do much more research than I ever could.

4. Investing in Liquidity Pools

Liquidity pools are a yield-generating investment brought about by Automated Market Makers (AMMs) like Uniswap. AMMs, allow for token holders to trade currencies and tokens without a traditional order book or even direct connection between a buyer and a seller. These token exchanges allow users to trade tokens quickly and transparently. To achieve this kind of liquidity, the exchange sets up token pools to back the trades instantly. In this way, users wanting to trade do not need to achieve a peer-to-peer exchange through an order book; instead they can do a peer-to-pool contract exchange, instantly. Investors willing to provide liquidity to the pool are rewarded with fees in form if tokens issued by the exchange (eg: UNI tokens for Uniswap pools)

Liquidity pools are setup across common token pairs (eg: EHT<> USDC) and liquidity providers (aka the investor) is rewarded proportionally to the stake they hold in the pool. Some token pairs are rewarded more than others based on trading demand (more trades, means more fees) and liquidity in the pool. Some of the most lucrative pools estimate an eye-popping 43% in annualized returns… seems too good to be true…

I’ll admit that at this point I do not understand how to figure out the best pools to provide liquidity to... that may be a good topic for a future post.

Lets analyze investing in liquidity pools:

How is value generated? Fees generating by trades are distributed back to the liquidity providers in the form of tokens

Risk: If the price of the token you provide to the pool the changes significantly you are exposed to impermanent loss4. I have a hard time understanding this concept… for that reason I will consider it high risk

Upside: 0-49% depending on the token pair. This seems too good to be true! true annualized yields are unlikely to keep up with these estimates by the exchange.

Security: Exchanges have been attacked before. As with tokens, good security audits, time in market, and total locked up value in pools are good indicators that the service is secure.

Regulatory: In this case, the exchange is totally transparent, fees are clear to the users of the exchange and it is hard for one user group to take advantage of another since there are no humans in the middle. If impermanent loss becomes a pervasive risk wiping out liquidity providers en-masse, regulators could step in.

Maintenance: Very high. Tracking token price and fees generated are a must. Hopping across pools to follow yields is common practice.

5. Automated yield farming

Automated yield farming is one the newest categories of DeFi services, and I’ll admit, a bit of a mind-bender. It’s like a robo-investor for your crypto assets mixed in with community voting and insurance.

The best known service for automated yield farming is Yearn Finance, which allows investors to deposit their crypto currency into a pool, which is then algorithmically managed to optimize yield. They call these pools Vaults. Yearn combines some of the approaches discussed earlier to generate yield: They provide liquidity in other pools, leverage the capital at low borrowing cost in a specific token to then loan out a larger amount with a higher return based on current market conditions, and more techniques I don’t fully understand. All of this is automated for the investor with promises to minimize risk while maximizing yield. Yearn also sells insurance on the investment if you want to minimize the risk further.

There are two additional interesting mechanics. First, Investors in Yearn’s pools are issued pool tokens that represent their share of the pool. Second These tokens can be used to vote for and direct investment by Yearn. The tokens themselves can be sold to other investors. I don’t yet understand the implications of tokenizing the investment… again another opportunity for a deep dive post.

While I don’t fully understand how Yearn works, intuitively I love the idea of algorithms pouring across the vast amount of open exchanges and lending protocols, finding the most timely opportunities and directing your investment there. In DeFi, there is no need for “insider information” because most information is readily available. There is just so much of it, and evolving so quickly, that algorithms are far better positioned to make optimal decisions than humans. I’m very intrigued by automated yield farming.

Lets analyze automated yield farming:

How is value generated? A combination of DeFi investment techniques like liquidity pools, lending and others.

Risk: Hard to quantify. If the algorithms are sound, it’s likely lower than any individual approach on a given token (big IF)

Upside: The value of the pool tokens has grown by as much as 50% in a few months. Yearn does not provide clear yield metrics, because they don’t issue back the yield, they just increase the total value of the pool (of which you own some portion) with the earnings.

Security: Likely similar to other DEXes. The investments themselves are likely lower risk as they are spread across various assets.

Regulatory: This approach is so new that it’s unlikely to get the attention of regulators soon. However an overall crackdown of DeFi would affect the underlying assets they invest in.

Maintenance: Low, in the long term, high at first. Because it is hard to understand how the protocol works and it’s a new product, I would want to check in frequently until I understand it better.

Congratulations mortal, you made it to the end of the DeFi deep dive! Time to come out of the pool and take a deep breath.

Personally, I have begun to understand what many of the buzz words thrown around in DeFi mean and I can now take the time to do some reflection and decide which of these investments I would make given my personal circumstances.

In the next Crypto for Mortals…

I will explain how I arrived at an investment decision and will outline how I made the investment/s.

In the meantime, I would greatly appreciate it if you can add comments with questions, suggestions or corrections I should make. Your feedback helps me get better.

Until then, stay curious!

And as always, this post should not be treated as financial advice, only my personal opinions. Please seek professional financial advice if you intend to invest.

KYC - Know your Customer requirements:

Gracias again Agus. Question on “liquidity”: you don’t mention liquidity so I assume any of these investment possibilities are all 100% “liquidable”?

Congratulations ! Most comprehensive guide to Defi I have ever read!